Blog

Articles on edge, backtesting, and validation.

How many trades do you need to validate a trading strategy?

A strategy reaches full statistical weight in Quantprove at 500 trades. Below that, the confidence multiplier discounts the score. Here is how to read a thin sample.

How to know if your trading strategy will pass a prop firm challenge

Most challenges end at the drawdown limit during a normal losing streak. Estimate your pass probability from your own trade history before you pay the evaluation fee.

How to know if your trading strategy has a real edge or just got lucky

A real edge survives a large sample, a significance test, out of sample data, and a Monte Carlo resample. A lucky streak passes one of these and fails the rest.

Why your live results don't match your backtest

Some gap is normal. A large one has a cause: overfitting, missing costs, execution friction, or a regime shift. How to name yours and measure it.

How to know when your trading strategy stops working

A losing streak ends. A dead edge does not come back. The structural reads that separate ordinary variance from real edge decay.

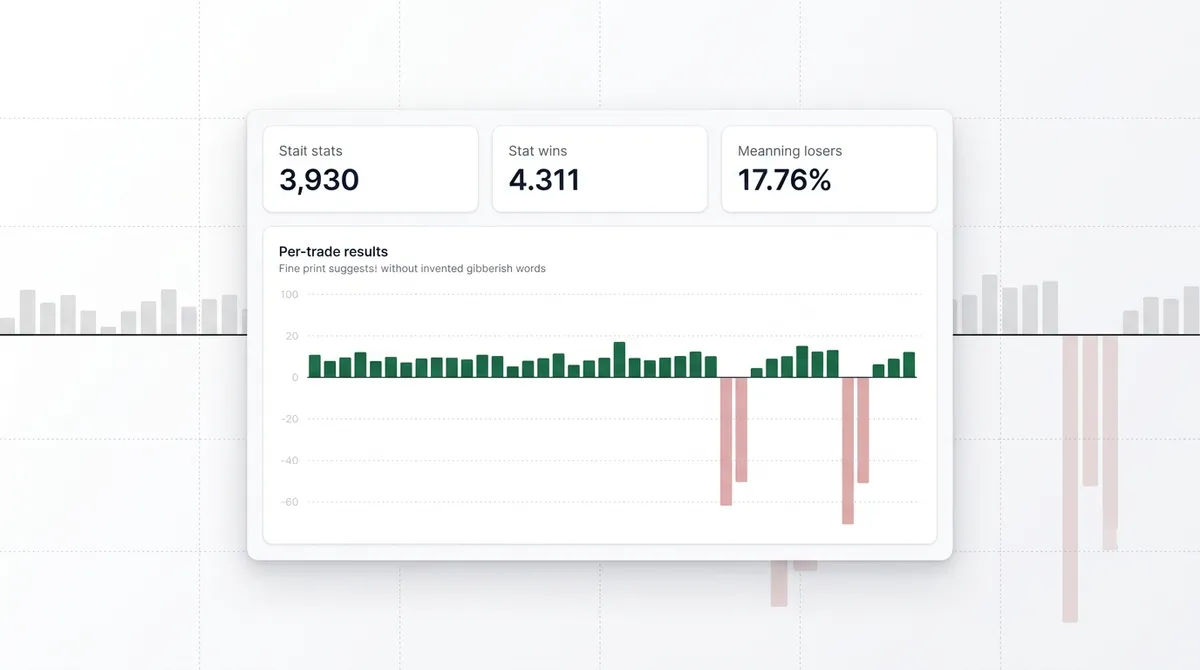

Why a high win rate can still lose money

Win rate says how often you are right. Expectancy says how much being right is worth. A 90% winner with a deep losing tail is a losing system wearing a good record.

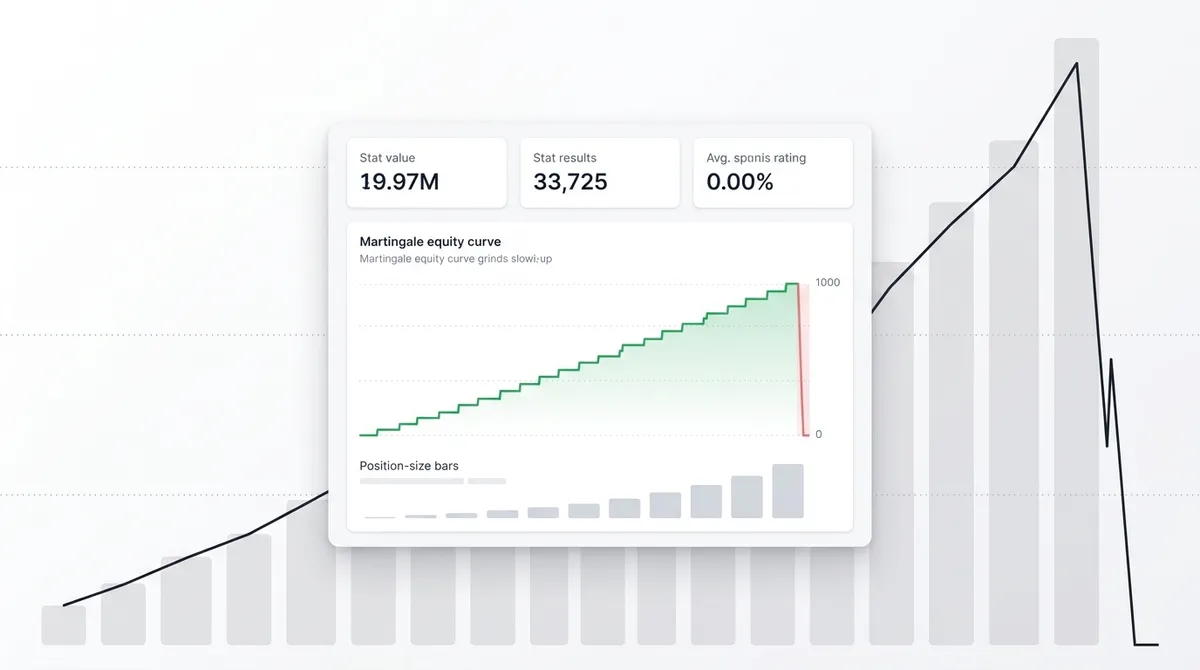

Why martingale strategies blow up accounts

Doubling after losses converts a high win rate into a scheduled meeting with your account's limit. The math, the perfect looking curve, and how to spot it in a track record.

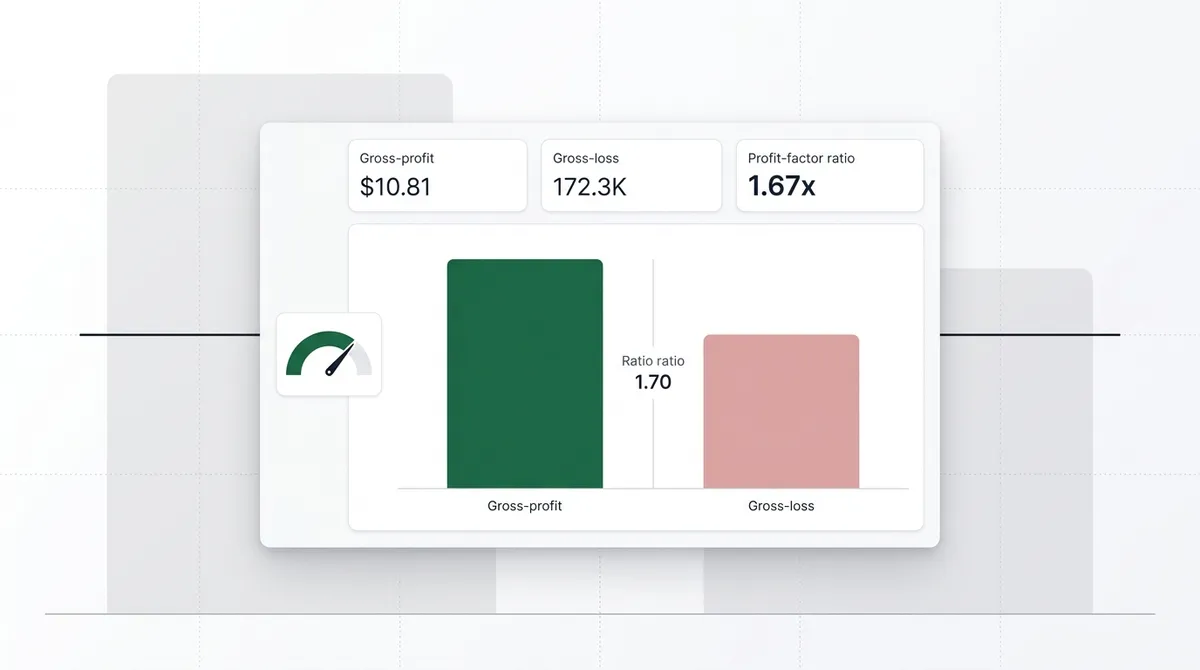

Profit factor explained, and why it is not your edge

Profit factor is gross wins over gross losses. It is useful, easy to inflate, and not the same as having an edge. Here is what it misses.