Glossary

Everything explained, in one place.

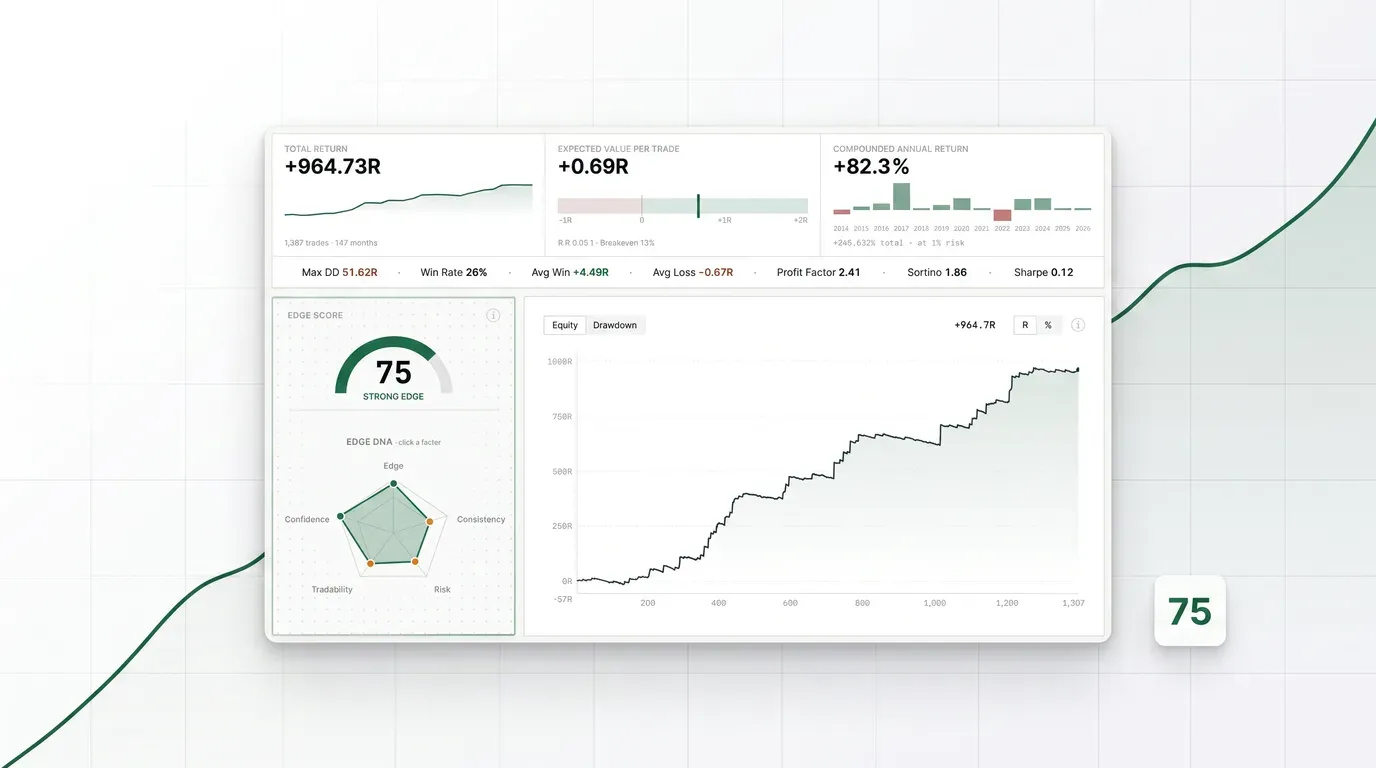

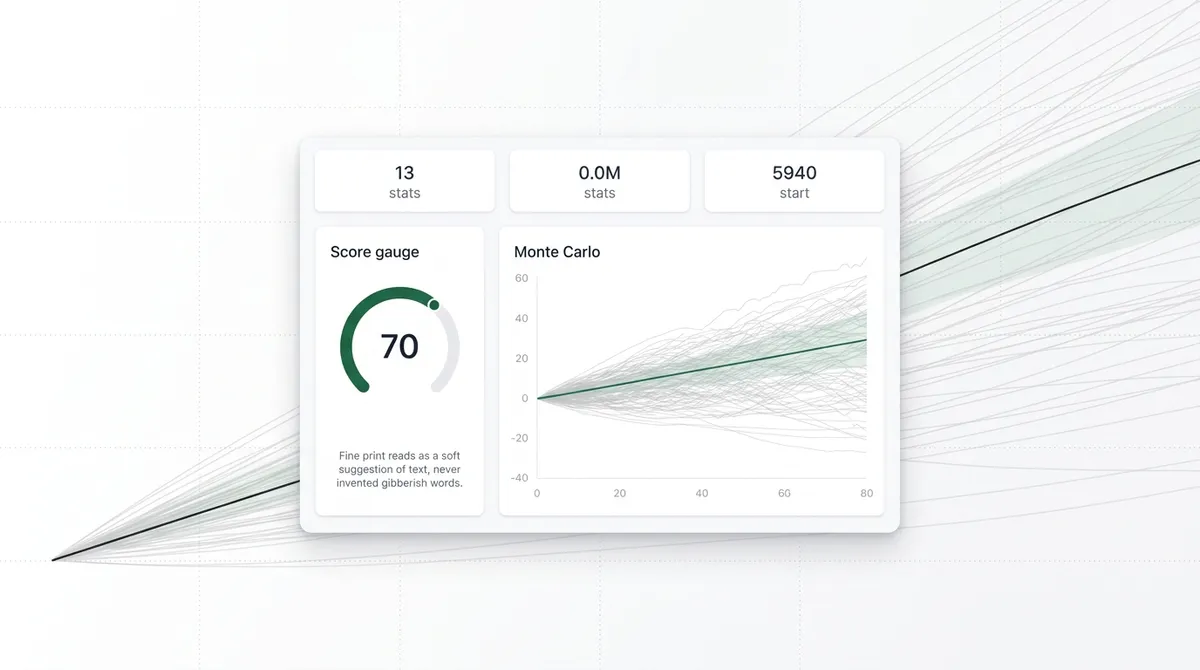

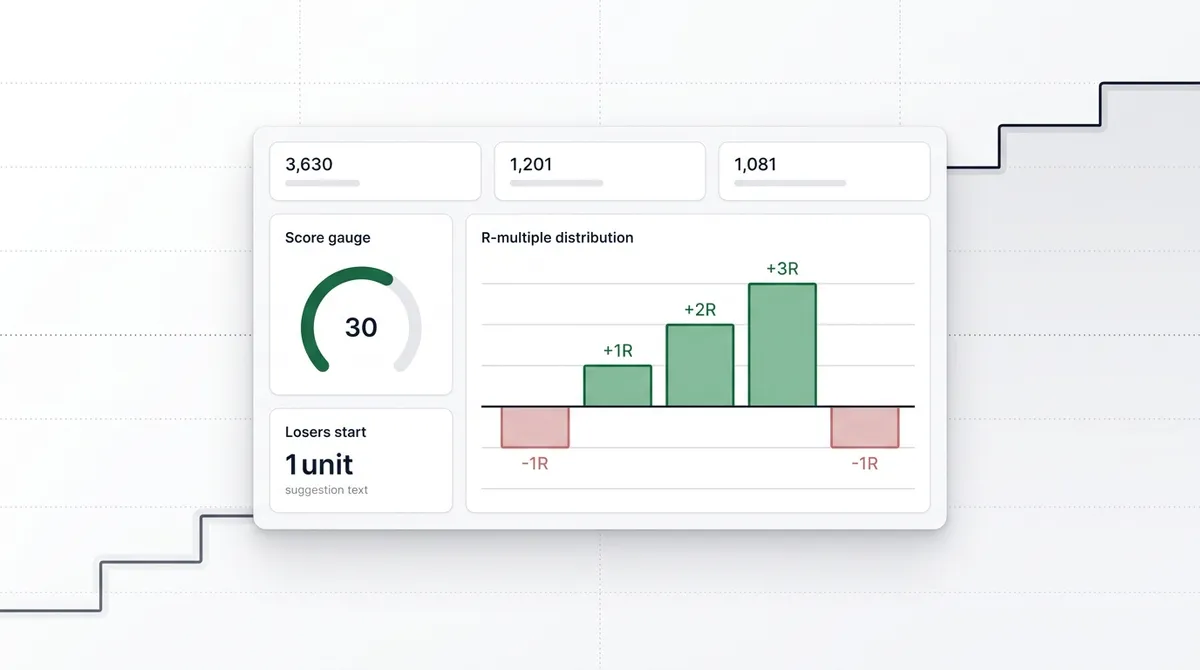

Edge Score

Quantprove’s 0-100 grade for a strategy’s statistical edge on historical data, scored across four weighted buckets.

Stability Score

Quantprove’s 0-100 grade for whether your live results still match the backtest distribution out of sample.

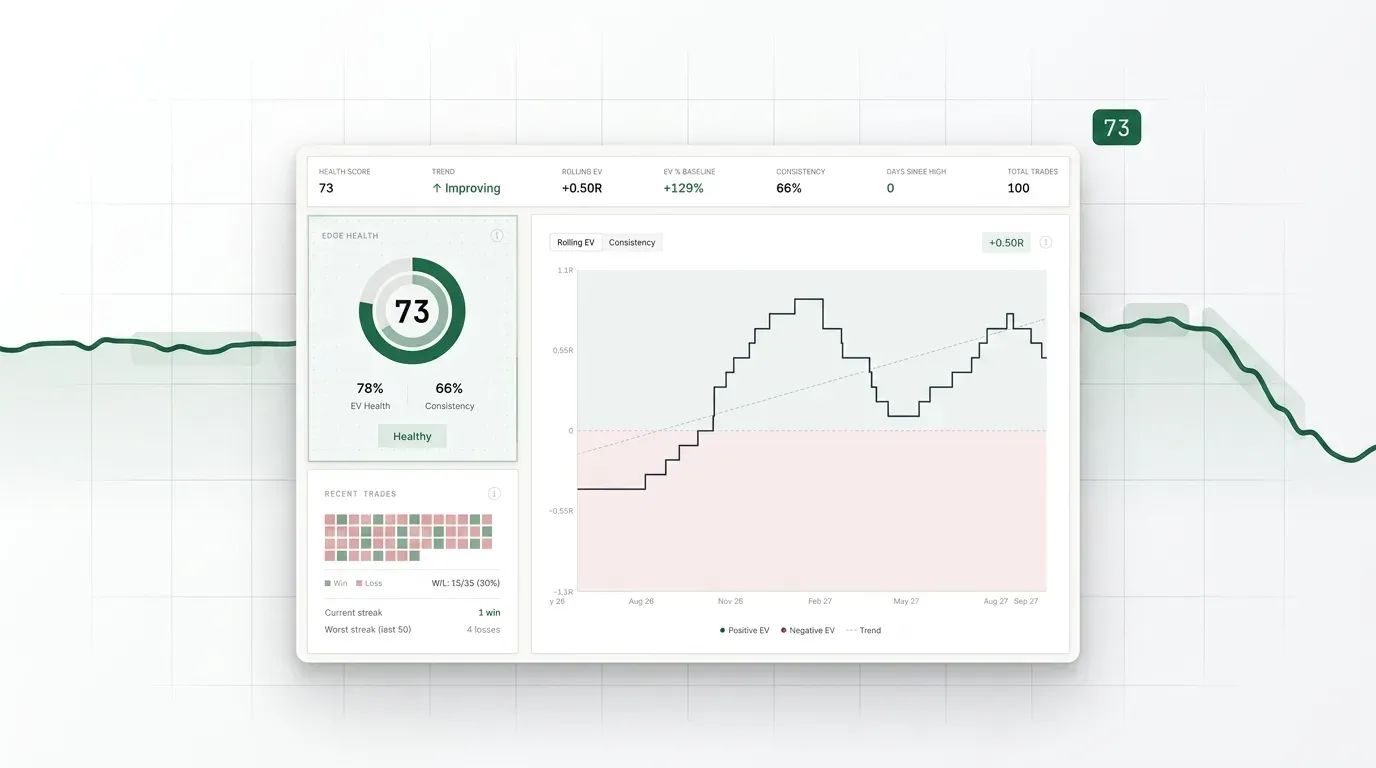

Health Score

A 0-100 combined score that shows whether a live strategy’s edge is still holding or quietly decaying over time.

Overfitting

When a strategy is tuned so tightly to past data that it captures noise instead of a real edge, and falls apart live.

Expectancy

What a trading strategy makes per trade on average, once its wins and losses are netted out.

Sortino Ratio

A risk adjusted return that judges a strategy only on its downside swings, not its upside.

Maximum Drawdown

The largest peak to trough drop in an equity curve, the worst losing stretch a strategy has handed you.

Monte Carlo Simulation

Reshuffling your trades thousands of times to map the range of outcomes your edge could produce.

R Multiple

Each trade measured as a multiple of the risk you took, where a full stop out is always minus 1R.