Best Practices

Guides for uploading data and reading your scores.

How to upload your trade data to Quantprove

Upload format, R-multiple vs dollar detection, and the minimum data each mode needs.

Reading your Edge, Stability, and Health Scores

What the Edge Score, Stability Score, and Health Score mean, and how they connect.

Key metrics: EV, Sortino, drawdown, R-chart

EV, Sortino, CVaR, drawdown and retention, plus the R-chart, benchmark, and projection.

Common mistakes that distort a backtest

Thin samples, overfitting, unit/deposit distortion, and R-multiple annualization.

6 mistakes that most often inflate an Edge Score

The six backtest mistakes that push an Edge Score above the real edge, and the check that catches each one.

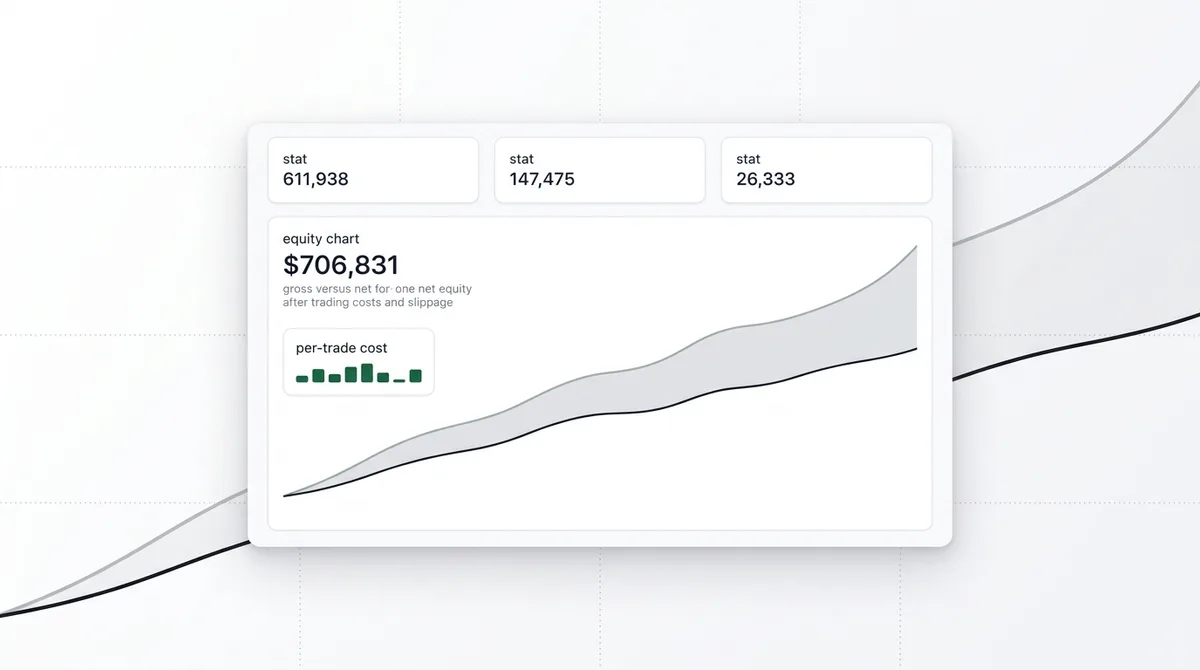

How to build trading costs and slippage into your backtest

Commissions, spread, slippage, and swap each take a slice of every trade. How to model them per trade and rebuild your backtest net.

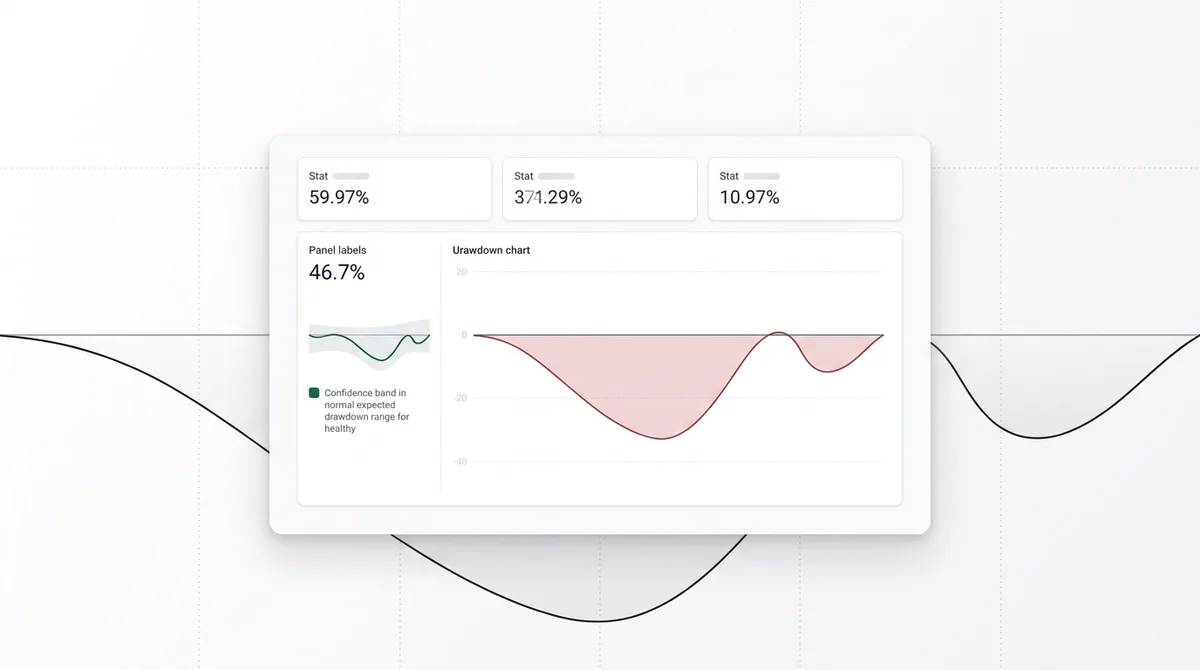

How to know if a drawdown is normal or your edge is gone

Your backtest and a Monte Carlo range define what a normal drawdown looks like. How to read depth, duration, and streaks against your own bounds.

How much should you risk per trade

No universal number. Size from your loss streaks and drawdown profile, then test the level on your own trades before trading it.

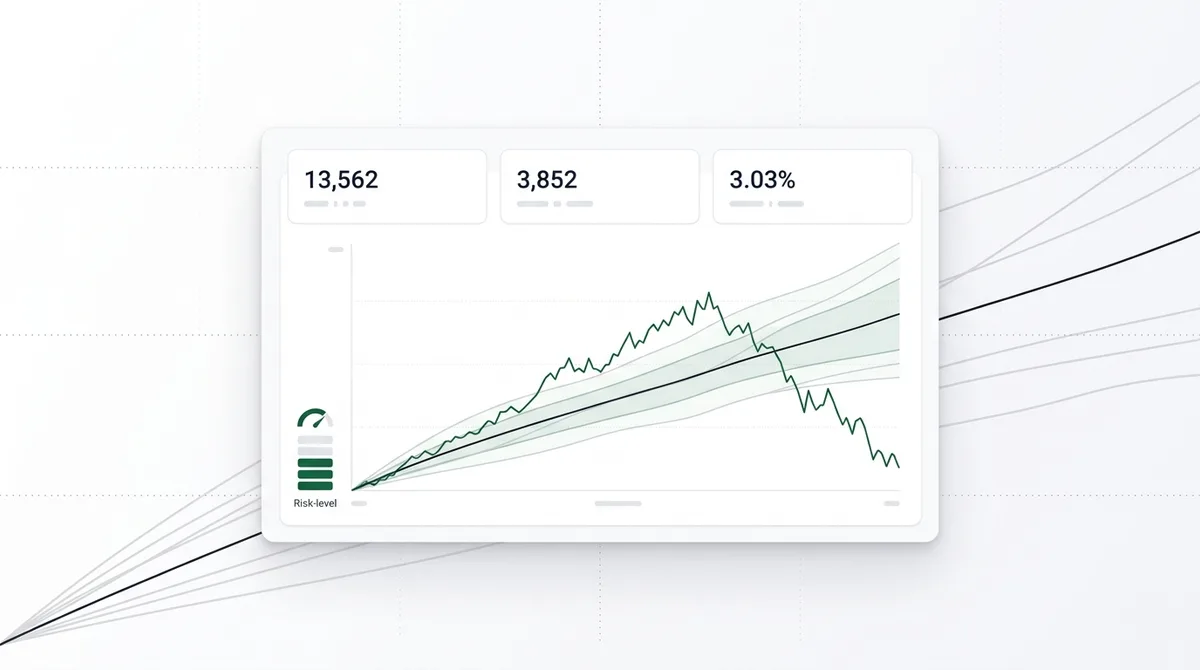

What is risk of ruin and how do you calculate yours

The probability your account ever hits its floor, the four inputs that drive it, and how to read yours from your own trades.

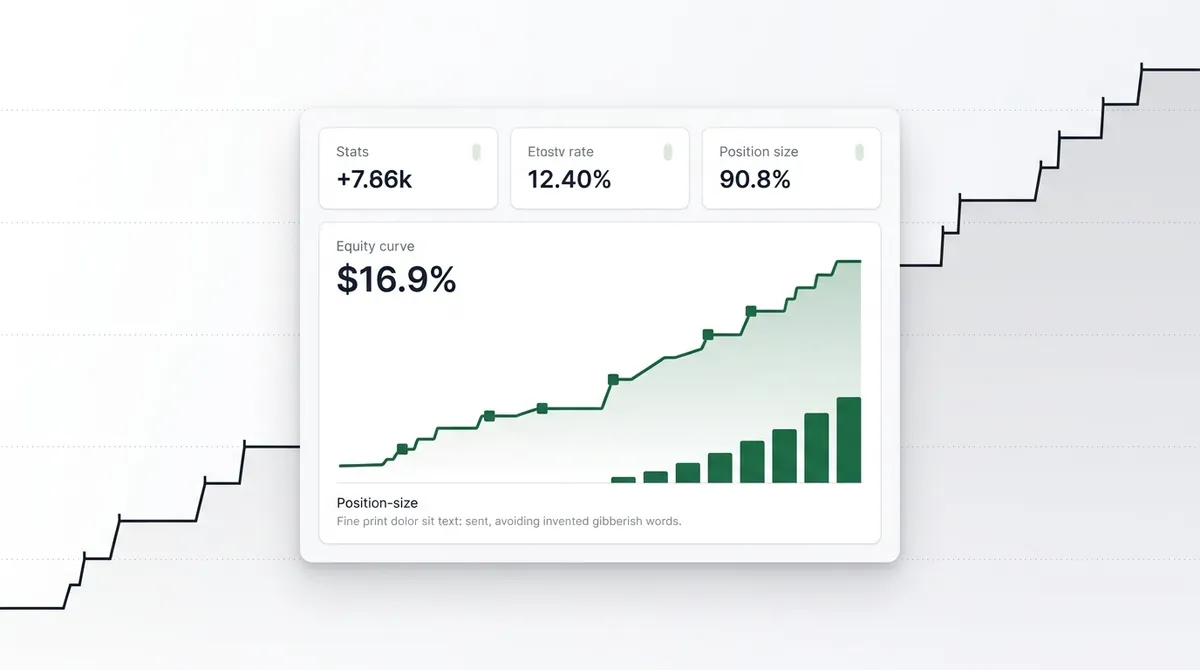

When should you increase your position size

Scale when the evidence grows, not when confidence does. The three gates a size increase has to clear first.

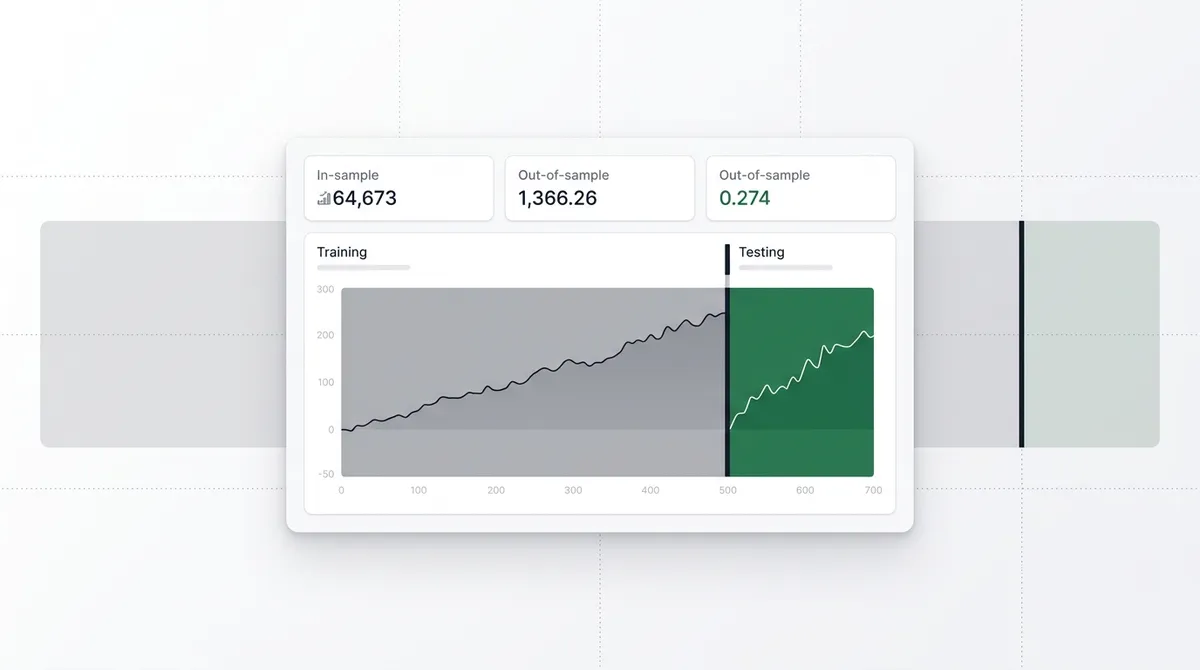

How to test a trading strategy out of sample

Hold back data the build never touched, run the rules unchanged, compare distributions. The discipline that separates a tested edge from a fitted one.

Walk forward analysis, explained for real traders

How walk forward analysis tests a strategy on a rolling basis, the way you actually trade it, and where it still fails.